Ask most people what insurance they have, and they’ll tell you about their car insurance and their home insurance. Maybe life insurance if they have a mortgage.

Ask them about income protection, and you’ll usually get a blank look.

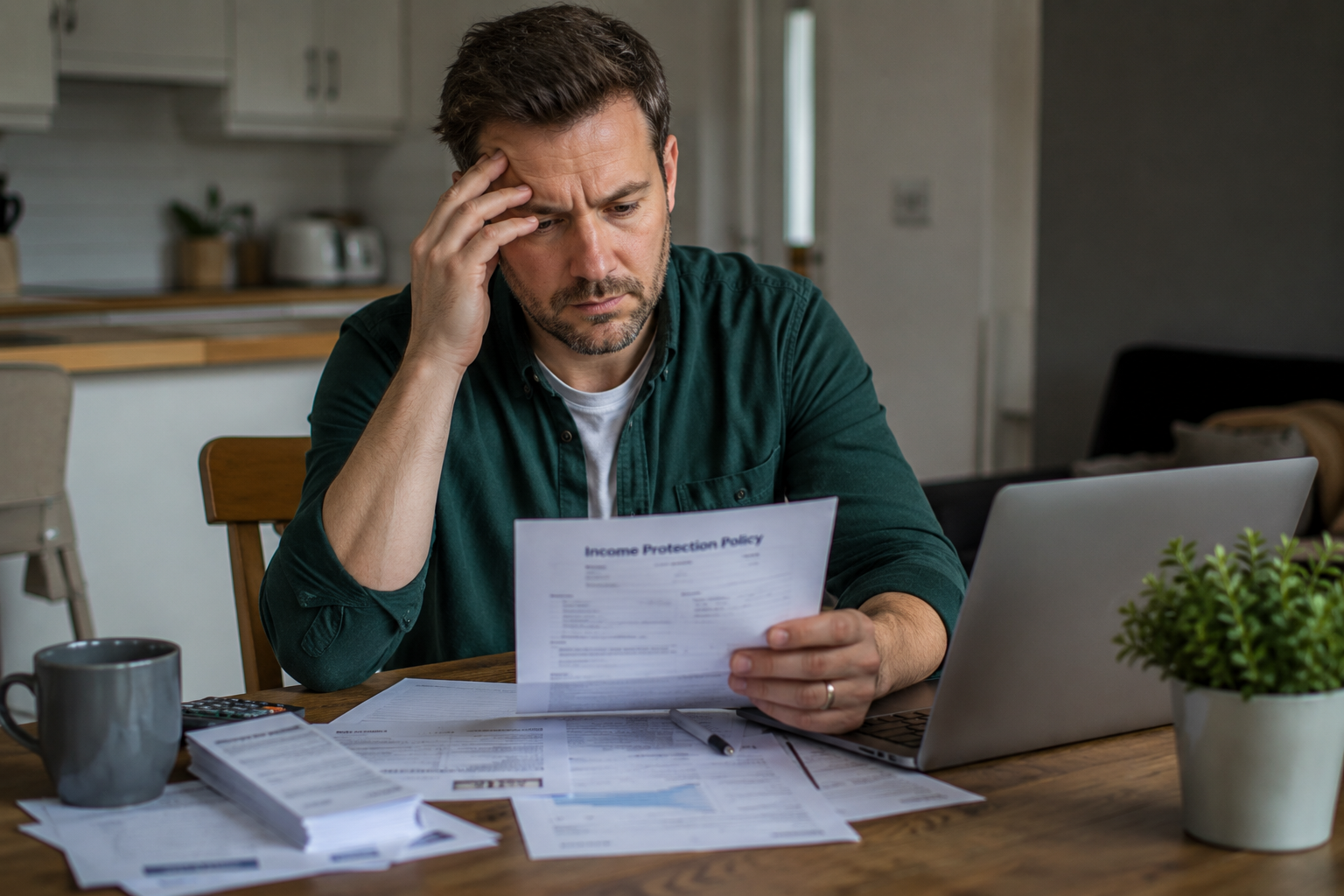

That’s a problem — because income protection is arguably the most important policy you can own, and the vast majority of working adults in the UK don’t have it.

Here's the thing nobody wants to say out loud

You are far more likely to be off work for an extended period due to illness or injury than you are to die during your working life.

The statistics back this up. Around one in four people will be unable to work for a month or more at some point in their career due to illness or injury. The average long-term absence lasts over a year. And yet income protection ownership in the UK sits at around 12% of working adults.

We insure the things we can see — the car, the house, the phone. We don’t insure the thing that pays for all of it.

"Statutory Sick Pay is £116.75 a week. Is that enough for your family to live on?"

What Statutory Sick Pay actually pays you

If you’re an employee and you go off sick, your employer is legally required to pay you Statutory Sick Pay for up to 28 weeks. The current rate is £116.75 per week.

Take a moment with that number. £116.75 a week. That’s roughly £505 a month.

The average UK mortgage payment is around £1,400 a month. The average rent in the UK is over £1,200 a month. Food, utilities, childcare, transport — add it up, and £505 a month doesn’t come close.

Some employers top up sick pay generously. Many don’t. And after 28 weeks, SSP stops entirely.

What income protection actually does

Income protection pays you a monthly benefit — typically 50% to 70% of your pre-tax income — if you’re unable to work due to illness or injury. It pays until you either recover and return to work, or until the end of the policy term, which can be your retirement age.

It’s not a lump sum. It’s a regular income replacement — the thing that keeps your mortgage paid and your family fed while you’re focused on getting better.

The best policies pay out on an own occupation basis, meaning they pay if you can’t do your specific job — not just any job. That distinction matters enormously. A surgeon with a hand injury can’t do their job, even if they could technically sit at a desk and answer emails. Own occupation cover would pay. A poorly-worded policy might not.

What about the deferred period?

Income protection policies have a deferred period — the waiting time between when you stop working and when the policy starts paying. Common options are four weeks, eight weeks, thirteen weeks, twenty-six weeks, or fifty-two weeks.

The longer you wait before the policy kicks in, the lower the premium. If you have savings or good sick pay from your employer, a longer deferred period can reduce your costs significantly. If you have nothing to fall back on, a shorter deferred period gives you faster access.

This is where advice makes a real difference. The right deferred period depends entirely on your personal situation, and getting it wrong means either paying more than you need to, or having a gap in cover when you need it most.

It's cheaper than most people assume

Because so few people buy income protection, there’s a widespread belief that it’s expensive. It isn’t, particularly when you’re young and healthy.

A 35-year-old in good health can often get income protection covering £2,000 a month for under £30 a month. That’s less than a gym membership most people aren’t using.

Premiums rise with age and vary significantly with health and occupation. The earlier you sort it, the cheaper it is — and the more likely you are to be insurable without exclusions.

Self-employed? It matters even more

If you’re employed, SSP is a thin but real safety net. If you’re self-employed, there’s nothing. No SSP, no sick pay, no employer top-up. If you can’t work, the money stops — immediately.

For self-employed people, income protection isn’t a nice-to-have. It’s the only version of sick pay that exists.