You’ve done the right thing. You’ve sorted your life insurance. You’ve picked the right amount, you’re paying the premiums every month, and you have the peace of mind of knowing your family is covered.

There’s just one problem. If your policy isn’t written in trust, the money might not reach your family for a very long time.

What is probate?

When someone dies, their assets don’t automatically pass to their loved ones. The estate — everything the person owned — has to go through a legal process called probate before it can be distributed.

Probate involves applying to the court for the legal authority to deal with the estate, paying any inheritance tax that’s due, notifying creditors, and then distributing what’s left to the beneficiaries.

In 2023, the average time to complete probate in England and Wales was around nine to twelve months. For more complex estates, it can take significantly longer.

"Nine to twelve months. That's how long probate takes on average. Is your policy set up to avoid it?"

What does probate have to do with life insurance?

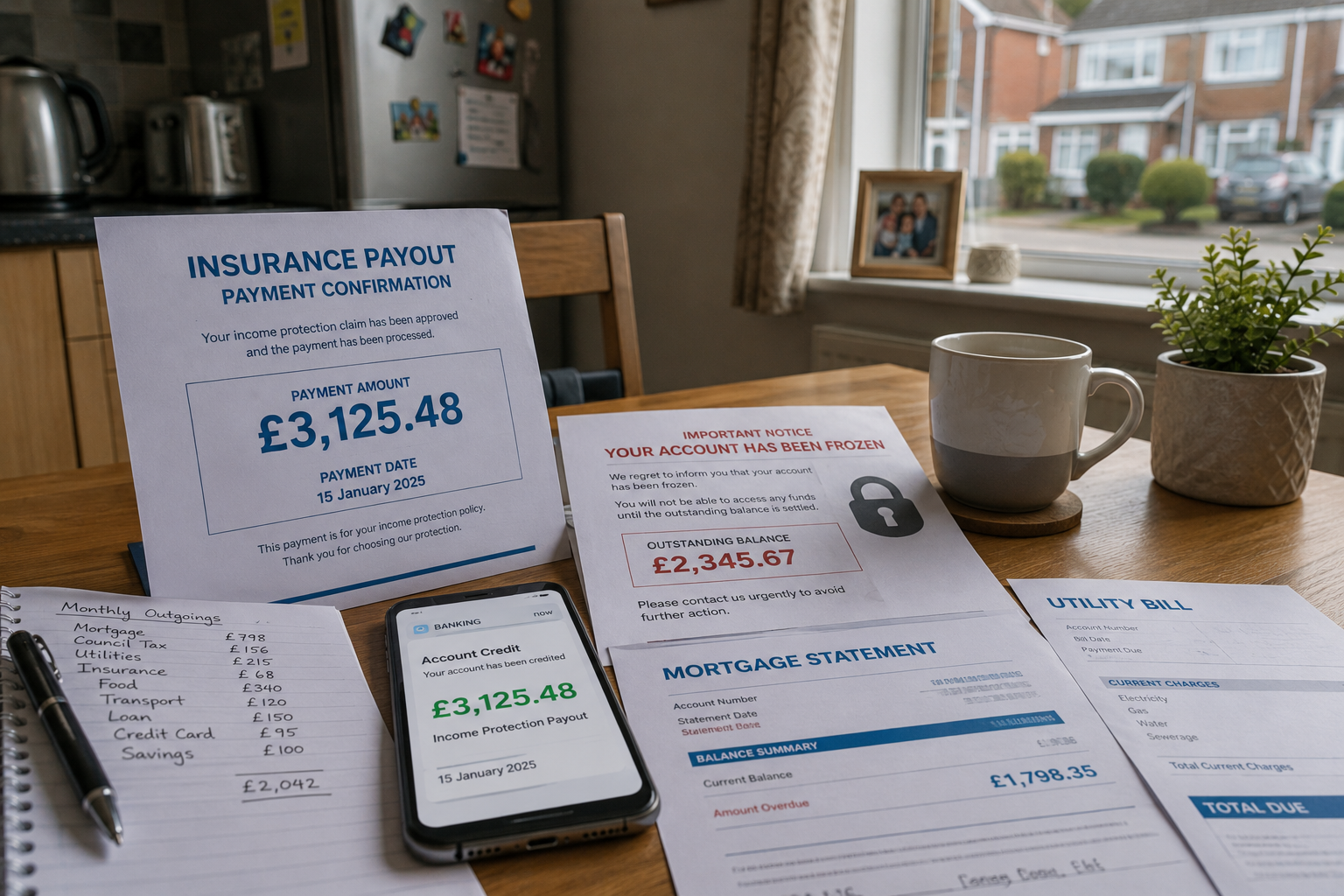

If your life insurance policy is not written in trust, the payout forms part of your estate when you die. That means it goes through probate along with everything else.

Your family can’t access that money until probate is complete. If probate takes nine months, the life insurance payout is frozen for nine months. During that time, your family is managing without you and without the money that was supposed to support them.

The mortgage still needs paying. The bills don’t pause. The kids still need feeding and clothing and looking after. And the financial safety net you put in place is sitting inaccessible in a legal process.

The inheritance tax problem

It gets worse. Assets inside your estate are subject to inheritance tax above the nil-rate band, currently £325,000 (or more with the residence nil-rate band). If your life insurance payout is inside your estate, it could push the estate above the threshold and trigger a 40% tax charge on the excess.

A £500,000 life insurance payout that goes into an estate already worth £200,000 could result in a significant inheritance tax bill. Your family receives less than you intended, and part of what you worked hard to provide goes to HMRC instead.

What writing in trust does

A trust is a legal structure that sits outside your estate. When you write your life insurance policy in trust, the payout goes directly to the trustees — who then distribute it to your beneficiaries — without going through probate.

This means the money can typically reach your family within weeks of a claim being settled, rather than months. It bypasses the probate process entirely. And because it sits outside your estate, it’s not subject to inheritance tax in the same way.

The practical difference is enormous. A family waiting nine months for funds versus a family who receives the money in two to four weeks — that’s the difference between managing through grief and financial crisis happening simultaneously.

So why doesn't everyone do this?

Largely because nobody tells them to.

Policies sold through comparison sites, banks, and direct insurers are rarely set up in trust as a matter of course. The process works, the premiums get collected, and the technical detail of how the money gets paid out is left unaddressed.

Setting up a trust is not complicated. It involves completing a trust form — provided by the insurer — and naming your trustees and beneficiaries. Most insurance companies provide their own trust forms at no charge. The whole process takes around twenty minutes.

What if you already have a policy that's not in trust?

You can usually still write an existing policy in trust, as long as you’re in good health and the policy terms allow it. It’s never too late to fix this, and it’s one of the most valuable twenty minutes you can spend.

If you’re not sure whether your existing policy is in trust, check your policy documents or call your insurer and ask directly. The question is simple: “Is this policy written in trust?”